[I]t is possible to see financial markets as a laboratory for testing hypotheses, albeit not strictly scientific ones. (p.14)「自反理論」並非狹義的技術分析或基本分析理論,而是更為廣義的哲學或社會學理論。雖然 Popper 早已意會到 Oedipus effect ── 亦即「自我應驗預言」﹝self-fulfilling prophecy﹞ 或「自我失效預言」﹝self-defeating prophecy﹞ ── 會令社會事件難以預測,但他仍深信存在同樣適用於描述自然科學與社會科學發展的「統一方法」﹝unity of method﹞。索羅斯不贊同 Karl Popper 的想法 ,他有見社會事件會涉及人,人的感知便會影響事態,事態又會反過來影響人的感知,而往往人的感知又存有偏見,導致問題 ──

I was greatly influenced at the time by Karl Popper's ideas on scientific method. I accepted most of his views, with one major exception. He argued in favour of what he called 'unity of method' ── that is, the methods and criteria that apply to the study of natural phenomena also apply to the study of social events. I felt that there was a fundamental difference between the two: the events studied by the social sciences have thinking participants; natural phenomena do not. The participants' thinking creates problems that have no counterpart in natural science. (p.11-12)

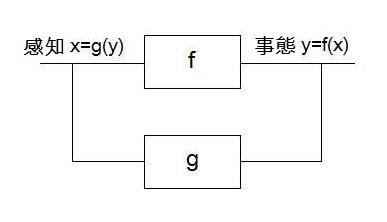

When events have thinking participants, the subject matter is no longer confined to facts but also includes the participants' perceptions. The chain of causation does not lead directly from fact to fact but from fact to perception and from perception to fact. This would not create any insuperable difficulties if there were some kind of correspondence or equivalence between facts and perceptions. Unfortunately, that is impossible because the participants' perceptions do not relate to facts, but to a situation that is contingent on their own perceptions and therefore cannot be treated as fact. (p.12)

I believed that the participants' bias is the key to an understanding of all historical processes that have thinking participants. (p.16)他將人的感知與事態的雙向反饋﹝double feedback mechanism﹞稱為「自反作用」﹝reflexivity﹞:

套用到金融市場,「不穩定」就是 boom and bust。索羅斯悟出:要在金融市場穩操勝券,須準確預期人對世事普遍會有什麼期望,而非真實世界會有什麼發生。他將此類操作稱為「煉金術」﹝alchemy﹞──

Scientific method seeks to understand things as they are, while alchemy seeks to bring about a desired state of affairs. To put it another way, the primary objective of science is the truth ── that of alchemy, operational success. In the sphere of natural phenomena, there is no distinction between the two objectives. Nature obeys laws that operate independently of whether they are understood or not; the only way man can bend nature to his will is by understanding and applying these laws. [...]But social phenomena are different: they have thinking participants. Events do not obey laws that operate independently of what anybody thinks. On the contrary, the participants' thinking is an integral part of the subject matter. This creates an opening for alchemy that was absent in the sphere of natural science. Operational success can be achieved without attaining scientific knowledge. By the same token, scientific method is rendered just as ineffectual in dealing with social events as alchemy was in altering the character of natural substances. [...]Financial success depends on the ability to anticipate prevailing expectations and not real-world developments. [...]Market prices always express a prevailing bias, whereas natural science works with an objective criterion. Scientific theories are judged by the facts; financial decisions are judged by the distorted views of the participants. Instead of scientific method, financial markets embody the method of alchemy. (p.303-304)或許你會認為索羅斯的「煉金術」與凱恩斯(John Maynard Keynes)的「鬥傻理論」﹝bigger fool theory﹞無異;在細節上,「煉金術」的重點在於識別可助長雙向反饋的條件,以股票市場為例,若然投資者的偏見不單令股價偏離合理值,且還影響到基本因素﹝例如因公司持有的股份價格上升而獲利、市值上升而有利拼購等﹞的話, boom/bust 就很可能會出現。更甚者,「煉金術司」還可施展「煉金術」,主動影響市場及其他投資者的感知,點石成金。

參考資料:

- The Alchemy of Finance: Reading the Mind of the Market, George Soros, John Wiley & Sons, ISBN 0-471-04206-4

- The Poverty of Historicism, Karl Popper, Routledge Classics 2002, ISBN 0-415-27846-5